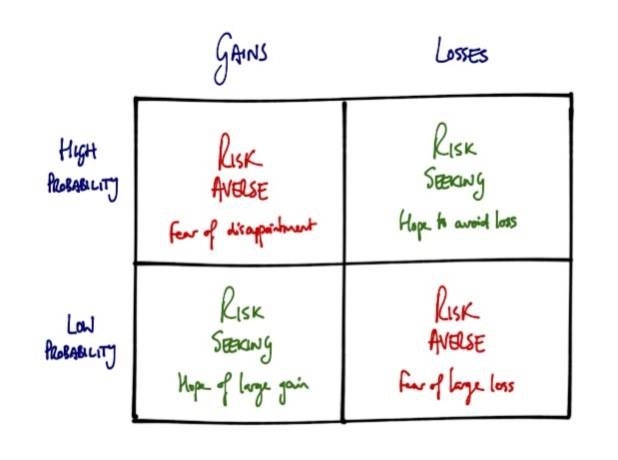

‘Prospect Theory’ or the ‘Loss-Aversion Theory’

02/06/2015

Evergreen Bangsar

03/06/2015

Top 5 Tips: Getting a Housing Loan

1. Know Your Financial Capacity

Think like lenders and evaluate the three things they consider when assessing loan applications: your income, your credit history, and your debt service ratio. Your income is important because it helps lenders determine your capacity to repay a loan, while your credit history shows that you can properly manage your finances. Debt service ratio refers to the proportion of your monthly take-home pay that will go to your monthly amortization. As a rule of thumb, you should not spend more than 30% of your income on housing.

2. Determine the Amount You Should Borrow

Aside from your paying capacity, the loan amount is also determined by the property’s appraised value. An important thing to remember: borrow only the amount you can pay back to avoid facing foreclosure and losing your investment altogether.

3. Study Your Financing Options

Now that you know what you can afford, it is time to evaluate which home financing scheme offers loan terms and monthly amortizations you can live with.

4. Bank Loans

Commercial and universal banks are home-buyers’ first resort when looking for housing loans. Compared to other lenders, banks grant longer loan tenure and more competitive interest rates. Although’ interest rates are adjusted after a certain number of years, the home-buyer will still pay lower monthly amortizations than they would under a developer’s in-house financing.

5. In-house Financing

Applying for in-house financing is simple and straightforward. Most of the time, developers require nothing more than the down payment and a verifiable proof of income, and little or no background checking is done. But this less stringent application process comes with a steep price: interest rates in in-house financing can be prohibitive and loan tenure is short, rarely exceeding 10 years.