Who doesn’t want to pay off their home loan as quickly as possible? But it often feels like an uphill battle, with you eating away at what you owe oh-so-slowly over the long haul. How do you deal with this?

Use mortgage calculators

You won’t be able to make progress unless you know precisely what you owe, and how much you can afford to adjust what you’re paying.

Give our repayments calculator a whirl to start you off – plug in how much more you think you can pay, and see what happens.

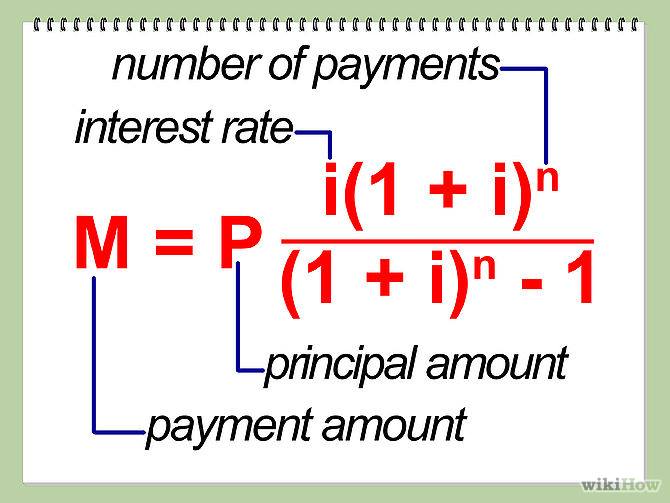

*The photo shows how to calculate mortgage interest

Pay fortnightly

Halving your monthly repayment and paying every fortnight lets you pay 26 rather than 12 repayments a year. That may sound like the same thing, but in fact you’ve added the equivalent of one extra monthly repayment every year on a principal and interest of your loan. That can add up to big numbers over the life of your loan.

Not all mortgage providers will let you make fortnightly repayments, so check first.

Utilise lump sums & windfalls

If you get a large tax return, bonus, inheritance or investment dividends, consider adding these to your mortgage account. With many home loan products, these can help reduce the amount of interest you’re paying significantly, cutting years off your repayment schedule overall.

Remember there are tax implications for these, so check carefully about any additional costs you might be obligated to pay.

Explore discount entitlements

Sometimes you can get discounts on your home loan if you’re a member of a certain occupation or professional organisation. Ask your lender if your profession entitles you to a different option and any additional savings. It never hurts to ask!

Consider updating your bank accounts

If your mortgage is your financial priority then it makes sense to make sure you are working it the best way possible to minimise interest. Talk to your bank manager to make sure you’re using your accounts the right way, sometimes a few tweaks can make a difference.

Review & compare regularly

Your needs change, your income changes, as do home loan products and interest rates. Don’t leave your home loan paperwork to gather dust and slip into a routine of automatic debits that you forget about. Stay on top of what you’re paying and how you’re tracking.

Work with your mortgage provider to develop a system for regular health checks on your loan, asking if there are better interest rates, better deals, different products that better suit where you’re now versus when you took out the loan.

Get frugal

The most obvious way to pay your place off faster is to cut back on other costs and invest that money into your loan fortnightly or monthly. If you can afford to take regular holidays (though you no doubt deserve them), think of how that money could be better spent invested in your loan.

When you’re mortgage free, the holidays should be all the more enjoyable!

Get it right before you start

If you haven’t bought yet, the single best way to pay off your property (if that’s your goal) is to be able to afford it. Take care not to overcapitalise when you buy, as miscalculations or stubbornness about what you can afford is a sure fire way to end up in a vicious repayment circle.

*The information in this article is of a general nature only and does not consider your personal objectives, financial situation or particular needs.

Vanessa Paech, Realestate dot com dot au